Have you used a Buy Now, Pay Later Service? You’re not alone.

1 in 4 Aussies Are In “Buy Now, Pay Later” Debt—What To Know Before Your Next Shopping Spree

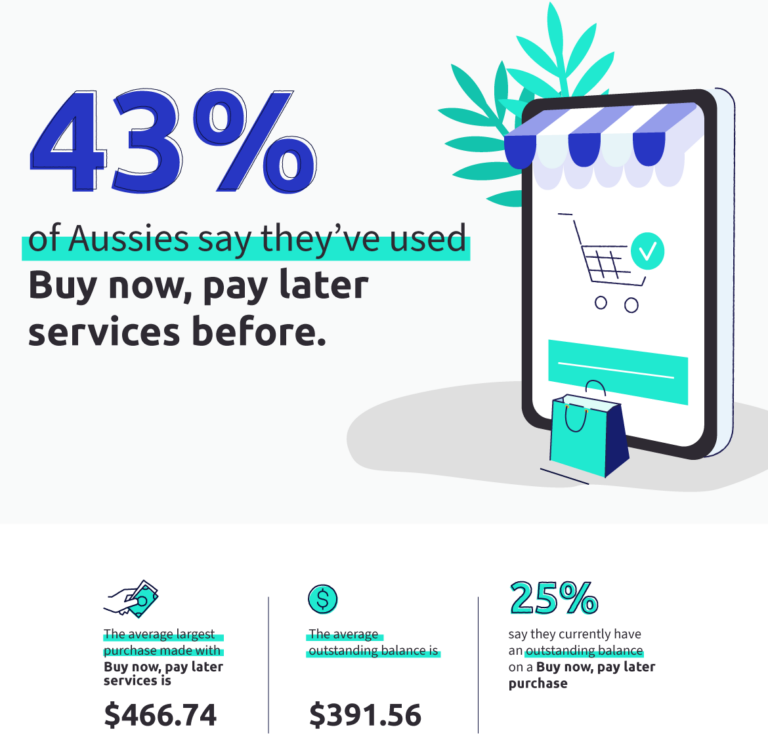

A quarter of Australians have a Buy Now, Pay Later (BNPL) debt outstanding, averaging $391.56.

BNPL services are on the up-and-up in Australia, and according to our survey 43% of Aussies say they’ve used a BNPL service before. On the surface, they offer convenience; instead of paying for your purchase outright, you can opt to go onto a payment plan to pay off your products over several weeks.

And with Christmas shopping looming ahead, it’s easy to see the appeal of delaying large payments in favour of smaller, manageable chunks. Especially if you’ve got your eye on a shiny new flagship phone, like the iPhone 13 or Samsung Galaxy S21, or even a new laptop.

Image source: Reviews.org

Why do we use Buy Now Pay Later services?

When it comes to why we want to use BNPL services, the answers are varied.

- 18% say they did not have enough money at the time to cover the full amount

- 16% say it’s easier to budget smaller payments

- 15% say they wanted to take advantage of a good timely sale

Many compared BNPL services to using a credit card.

- 11% say the fees and interest are lower than a credit card

- 8% say it’s more flexible than using a credit card

- 5% say because the approval process is easier than a credit card

Image source: Reviews.org

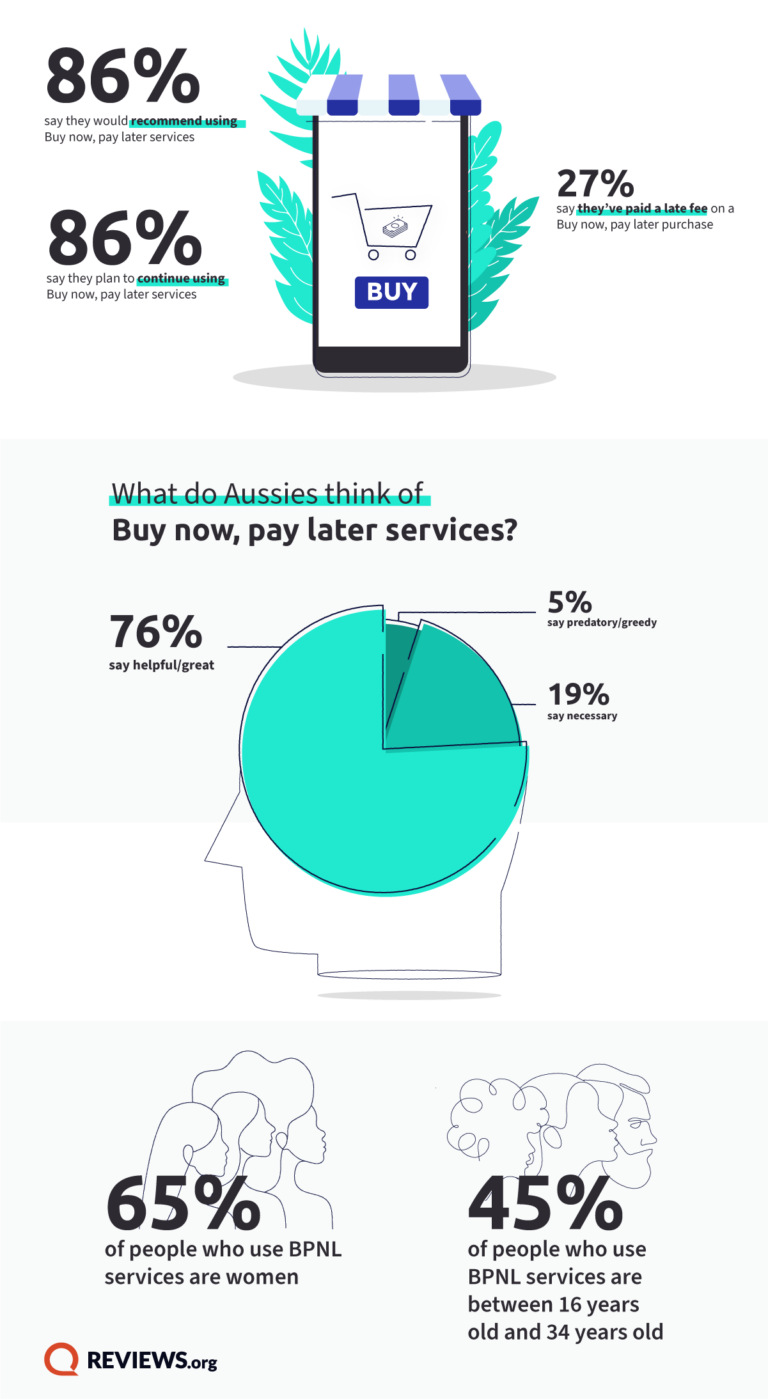

While BNPL providers don’t charge interest like credit cards do, they do charge fees, and these can add up if you miss payments.

However, we found that users look at BNPL providers favourably, with 86% surveyed saying they plan to continue using BNPL services, and 86% saying they would recommend using them. Only 5% thought that BNPL services were predatory or greedy.

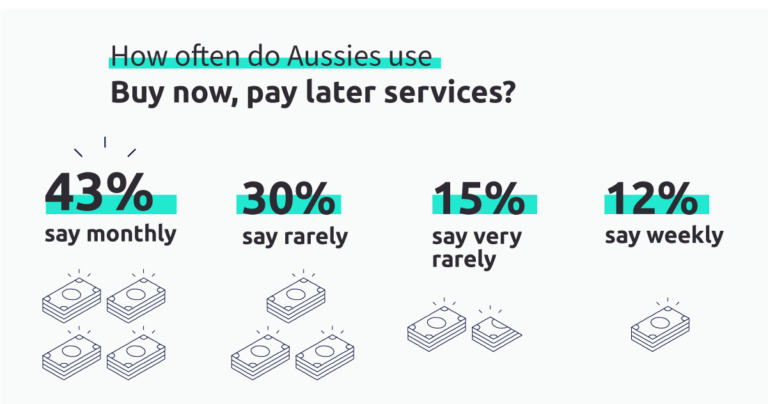

For many Aussies, using a BNPL service is a regular habit, with 43% of survey respondents saying they use BNPL services monthly. 12% said they use them weekly, while 30% said they use them just once or twice a year.

Image source: Reviews.org

Who’s using Buy Now Pay Later services?

It seems BNPL services are attracting a younger crowd. According to our survey, 46% of BNPL users are young people aged between 16 and 34 years old, and 65% of users are women. And when it comes to big buys, the average cost of large purchases made with BNPL services is $466.74.

Image source: Reviews.org

Proceed with caution

Despite an overwhelmingly favourable outlook from BNPL users, government website Money Smart says there’s a number of things to keep in mind when using BNPL services. In Australia, this includes companies like Afterpay, Brighte, Humm, Klarna, LatitudePay, Openpay, Payright and ZipPay.

- Watch your spending: it’s easy to overspend on things you can’t afford when you’re not paying for them upfront.

- Loan applications can be affected: just like any debt, lenders consider BNPL spending when you apply for a loan like a mortgage.

- Fees can add up: even if they don’t charge interest, double check the fees involved so you can stay on top of them

- It can be unmanageable: with so many BNPL services, if you sign up to several, it can be much harder to keep track of your payments, which could result in late payment fees.

Methodology

We surveyed 433 Australians about Buy Now, Pay Later services, then analysed the results for this report.

All figures are in $AUD.

Sources